Section 01

Total homeownersHow many Australians own their home?

The 2021 Census counted 10,852,208 occupied private dwellings across Australia. Roughly two in three were owner-occupied, split almost evenly between households that own outright and those still paying off a mortgage. The remaining third rent, either privately or through public housing.

The combined homeownership rate of 66% has been gradually declining from around 70% in the early 1980s, driven mainly by a fall in outright ownership as property prices rose and mortgage terms lengthened. Since 2003, more households have owned their homes with a mortgage than have owned their homes outright.

Section 02

Mortgage holdersHow many Australians have a mortgage?

Around 3.8 million households, or 35% of all occupied private dwellings, held a mortgage at the 2021 Census. The national median outstanding debt was $275,000 in 2019–20, with weekly housing costs averaging $493, about 16% of gross household income.

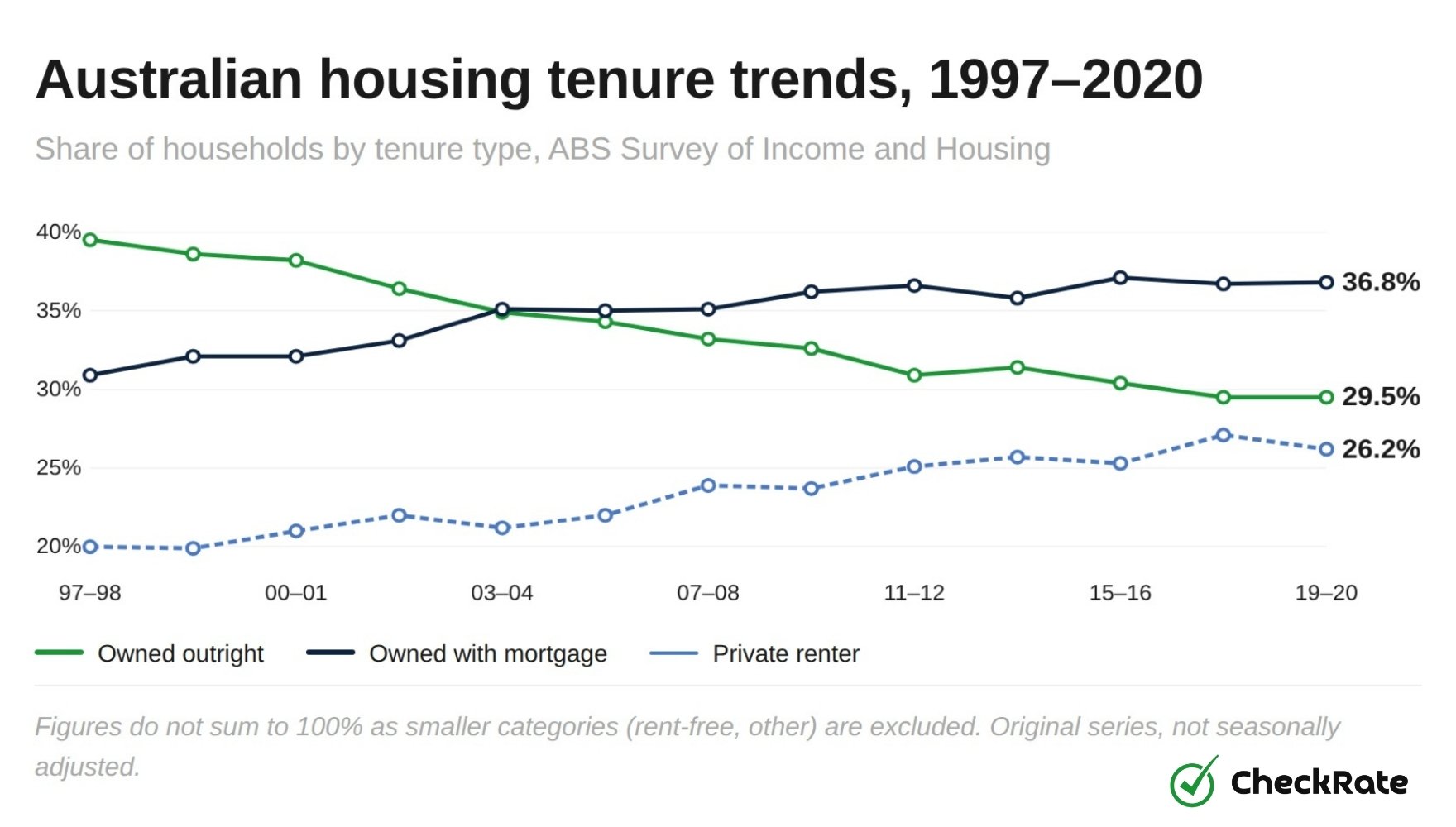

In 1997–98, outright ownership sat at 39.5% and mortgage ownership at 30.9%. By 2019–20, outright ownership had dropped to 29.5% while mortgage ownership climbed to 36.8%. Private renting has also grown steadily, from 20% to 26.2% over the same period.

New lending has picked up significantly. In 2025, there were 556,092 new owner-occupier and investor loan commitments, the highest annual total since the 2021 peak, with first home buyers accounting for 119,464 of those. The average new owner-occupier loan reached around $734,000 by the December quarter.

- Owned outright

- With mortgage

- Private renter

Section 03

Who is buyingWho is actually buying homes in Australia?

Age is the strongest driver of home ownership in Australia. Ownership rises sharply through people's 30s and 40s, then levels out in their 60s and 70s. More tellingly, every generation born since the mid-1950s has reached each age group with lower ownership rates than the generation before.

Australians born between 1947 and 1951 reached a 54.2% home ownership rate at ages 25–29. Those born from 1992 to 1996 had reached just 36.1% at the same stage of life, an 18 percentage point gap.

- 1947-51

- 1957-61

- 1967-71

- 1977-81

- 1987-91

- 1992-96

- First home buyers

- Changeover buyers

56.1% of first home buyers who purchased in the three years to 2019–20 were aged between 25 and 34, up from 49.6% in 2017–18. The share under 25 remained small at 5.3%.

Around 24% of changeover purchases in 2019–20 were made by households aged 65 or over, likely reflecting retirees using built-up home equity to downsize.

Section 04

Dwelling typesWhat types of homes do Australians live in?

Of Australia's 10.85 million private dwellings, separate houses make up the majority. The 2021 Census counted 7.7 million separate houses, roughly 71% of all homes. High-density apartments in buildings of nine or more storeys accounted for 394,303 homes nationally.

The state breakdown tells a clearer story. NSW has the highest share of flats and apartments, driven by Sydney's density. Victoria stands out for medium-density housing, with 237,779 one-storey townhouses, more than any other state.

Section 05

State by stateWhich Australian states have the highest home ownership rates?

Home ownership is not evenly spread across Australia. Rates range from 59% in the Northern Territory to 69.3% in Western Australia.

- Outright

- Mortgage

- Renting

| State / territory | Ownership | Mortgaged | Outright | Renting | Median mortgage | Cost % of income |

|---|---|---|---|---|---|---|

| New South Wales | 64% | 34% | 30% | 33% | $302,000 | 17% |

| Victoria | 68% | 37% | 31% | 29% | $285,000 | 16% |

| Queensland | 64% | 36% | 28% | 35% | $261,000 | 15% |

| South Australia | 69% | 39% | 30% | 28% | $216,000 | 14% |

| Western Australia | 69.3% | 42.7% | 26.6% | 28% | $280,000 | 14% |

| Tasmania | 68% | 35% | 33% | 29% | $177,000 | 15% |

| Northern Territory | 59% | 43% | 16% | 40% | $321,000 | 16% |

| Australian Capital Territory | 69% | 42% | 27% | 28% | $347,000 | 16% |

| Australia (national) | 66% | 35% | 31% | 30.6% | $275,000 | 16% |

- Northern Territory: the NT has the lowest overall ownership rate at 59% and the highest rental rate at 40%, reflecting the large share of public and community housing in remote areas.

- Western Australia: WA leads the country with a 69.3% ownership rate. Perth's median dwelling price rose from around $660,000 to $951,000 between 2023 and 2025.

- Tasmania: records the lowest median mortgage debt at $177,000 and the lowest average weekly cost at $346.

- ACT: highest median outstanding mortgage at $347,000 and the highest weekly mortgage cost at $546.

- Queensland and NSW: both sit at 64% ownership. NSW has the highest share of renters at 33%.

Section 06

AffordabilityHow affordable is it to buy a home in Australia?

Saving a deposit remains a decades-long challenge. In 2017, a single income earner saving 4.7% of their income needed roughly 25 years to save a 20% deposit. By 2025, even with a higher saving rate of 6.9%, the median dwelling price of $825,000 still leaves the timeline at around 21 years.

When household savings spiked to 13.9% during COVID lockdowns in 2020, the deposit timeline fell to around 8.3 years nationally.

Government programmes including the First Home Guarantee, shared equity schemes and state-based stamp duty concessions can help eligible buyers reduce upfront costs. But house prices have outpaced wages for so long that affordability is now a structural problem.

"Every birth cohort since the 1950s has entered each age bracket with a lower homeownership rate than the one before it. At ages 25 to 29, younger Australians are 18 percentage points below where the post-war generation stood."

References

- ABS 2021 Census of Population and Housing: housing tenure, dwelling counts and state breakdowns

- ABS Survey of Income and Housing: historical tenure trends 1997–98 to 2019–20, mortgage burden by state

- AIHW analysis of ABS Census data: home ownership rates by birth cohort and age group

- ABS Lending Indicators December Quarter 2025: annual loan commitments by borrower type

- RBA / APRA F6 Housing Lending Rates: average interest rates on outstanding and new mortgages

- ABS 2021 Census Administrative Data Snapshot: dwelling structure counts by type and state

- ABS Total Value of Dwellings: median residential dwelling prices by state

- ABS Australian National Accounts: household saving ratio and disposable income

- ABS Survey of Income and Housing 2017–18 and 2019–20: recent home buyers by age

Data Snapshots