Around 3.8 million Australian households have a mortgage. New owner-occupier loans averaged $736,000 nationally in the December 2025 quarter, rising to $873,000 in NSW. After the steepest rate-rise cycle since the early 1990s, average outstanding mortgage rates have eased from above 6% to 5.62%. Total new lending reached a record $385 billion in 2025.

10 min read 08 May 2026Updated 08 May 2026 Fact checked

Key findings at a glance

3.8M

Households with a mortgage at the 2021 Census, 35% of all occupied dwellings

$736k

Average new owner-occupier loan nationally, December quarter 2025

$385B

Total value of new home loan commitments in 2025 was a record high

5.62%

Average rate on outstanding owner-occupier mortgages, February 2026

Section 01Mortgage holders

How many Australians have a mortgage?

Australia had 10.8 million occupied private homes at the 2021 Census. Of these, around 3.8 million (35%) were owned with a mortgage, 3.36 million (31%) were owned outright, and 3.32 million (30.6%) were rented. Households that owned outright and those with a mortgage were roughly equal in number around 2003. Since then, more households have had a mortgage than owned their home outright, largely because rising property prices have extended repayment timelines and pushed more buyers into longer-term borrowing.

In 2019–20, the median outstanding mortgage balance nationally was $275,000. Weekly housing costs for mortgaged households averaged $493, equivalent to about 16% of gross household income. More recent lending data have since surpassed that baseline. By the December quarter of 2025, the average new owner-occupier loan had reached around $736,000, reflecting both higher property prices and larger borrowing amounts.

Households with a mortgage

3.8M

35% of occupied private dwellings · 2021 Census

Median outstanding balance

$275k

National median · 2019–20 ABS survey

Avg weekly housing cost

$493

For mortgaged households · 2019–20

Cost as % of income

16%

Share of gross household income · 2019–20

Australian housing tenure, 2021

Share of occupied private dwellings by tenure type

35%

have a mortgage

Owned with mortgage

35%

Owned outright

31%

Renting

30.6%

Other / not stated

3.4%

Source: ABS 2021 Census of Population and Housing.

A note on the data

The ABS cancelled its 2023–24 Survey of Income and Housing due to data quality concerns, which makes the 2021 Census the most reliable official baseline for tenure shares. The median outstanding debt and weekly cost figures come from the 2019–20 survey. Average new loan sizes come from the ABS Lending Indicators series, which is updated quarterly. Updated SIH results are expected around mid-2027.

Based on the 2021 Census, 35% of all occupied private dwellings were owned with a mortgage, covering around 3.8 million households. Among owner-occupier households, roughly 53% still carried a mortgage. In 2019–20, the national median outstanding mortgage balance was $275,000, while weekly housing costs averaged $493, equal to about 16% of gross household income. By the December quarter of 2025, the average new owner-occupier loan had reached around $736,000.

In 1997–98, outright owners made up 39.5% of households and mortgage holders 30.9%. By 2019–20, outright ownership had fallen to 29.5% while mortgage ownership had risen to 36.8%. The crossover occurred around 2003, as rising property prices contributed to longer repayment timelines. Private renting also increased over the same period, from 20% to 26.2%.

Section 02Loan sizes

How much do Australians borrow?

New loan sizes show how borrowing differs across Australia, with the largest loans concentrated in higher-priced housing markets. The national average for new owner-occupier loans reached $736,000 in the December 2025 quarter, but loan sizes vary widely by state. NSW borrowers averaged $873,000, compared with $504,000 in Tasmania. In most states, investor loan sizes sit close to owner-occupier loan sizes, reflecting where investors are active in the property market.

The data varies significantly by state. The selector below shows the current loan sizes and the 2019–20 cost data side by side. Note that the loan size and cost figures come from different reference periods.

Average loan sizes and mortgage costs by state and territory

New loan sizes · Dec 2025 qtr

Avg OO loan

$873k

Owner-occupier

Avg investor loan

$873k

Investor

Mortgage costs · 2019–20

Median outstanding

$302k

Avg weekly cost

$574

% of income

17%

Loan size data: ABS Lending Indicators, December Quarter 2025. Cost and debt data: ABS Housing Occupancy and Costs, 2019–20.

$369k

How much higher are home loans in NSW than Tasmania?

NSW borrowers averaged $873,000 in December 2025, $369,000 more than Tasmania’s $504,000. The gap between states is shifting, with rapid price growth in Perth pushing average WA loans from around $380,000 to $688,000 between 2022 and 2025, narrowing the gap with the eastern states.

For owner-occupier loans, the national average reached $736,000 in the December 2025 quarter, with NSW the highest at $873,000 and Tasmania the lowest at $504,000. Investor loans averaged $717,000 nationally. These figures refer to new loans written during the quarter. The median balance on outstanding mortgages was $275,000 nationally in 2019–20, the most recent comprehensive survey available.

Nationally, investor loans averaged $717,000 in December 2025, compared with $736,000 for owner-occupier loans. In NSW and Queensland, investor borrowing was close to owner-occupier borrowing levels. Investors also typically pay slightly higher rates: the APRA/RBA F6 series shows investor outstanding rates running 0.2 to 0.3 percentage points above comparable owner-occupier rates.

Section 03Lending activity

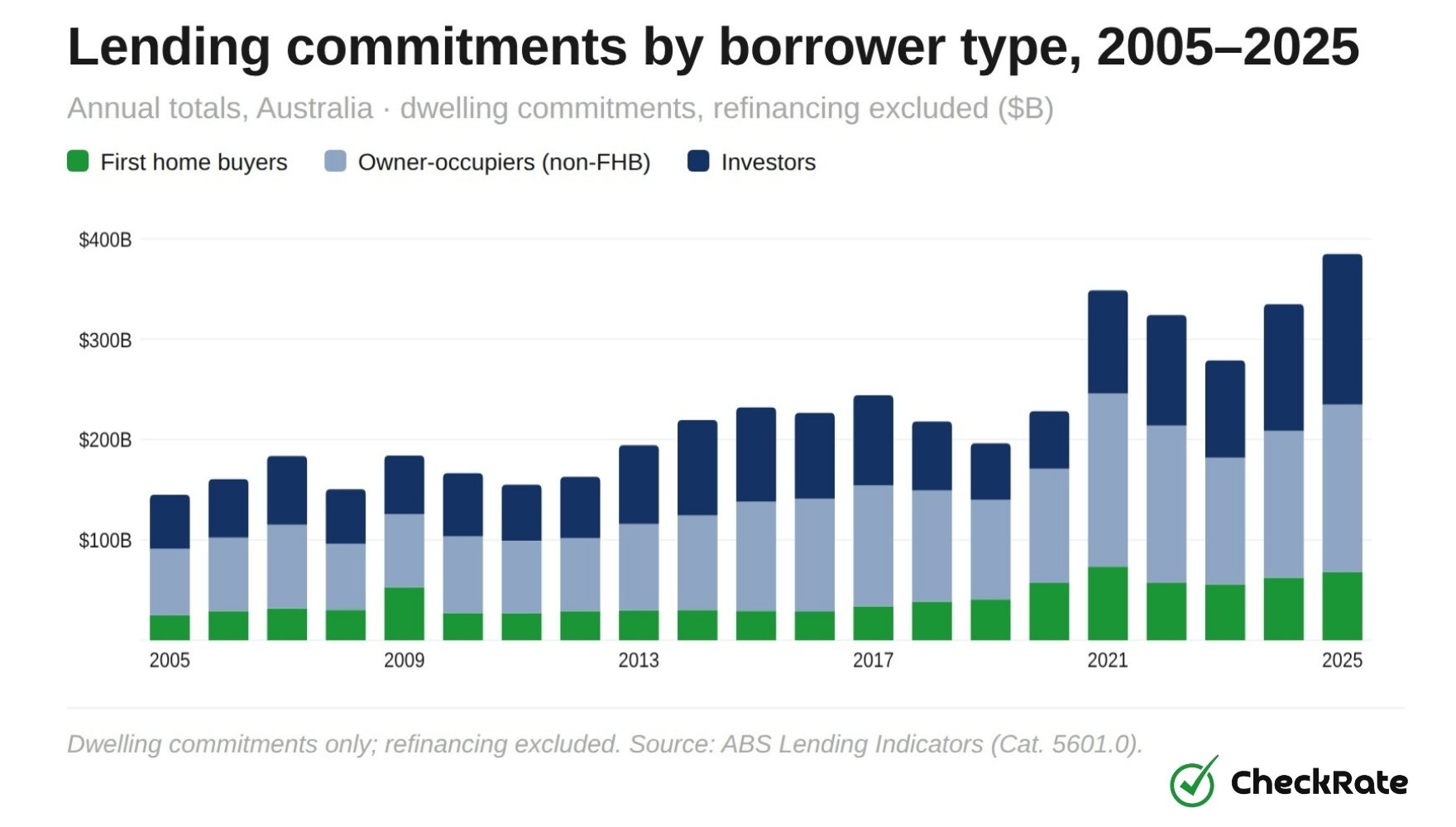

New home loan commitments from 2005 to 2025

Total new home loan commitments reached $385 billion in 2025, above the previous peak of $349 billion during the 2021 pandemic surge. The increase followed a sharp fall during the RBA’s rate-rise cycle, which began in May 2022 and saw total lending drop to $279 billion in 2023. Lending has since recovered, supported by more stable rates and later rate cuts.

Investor activity accounted for much of the increase. In 2025, investors committed to $150 billion in new loans, almost triple the $57 billion recorded in 2020 and the highest dollar value on record. First home buyers borrowed $68 billion in 2025, up in dollar terms but a smaller share of the overall market, as higher loan sizes and rate pressures limited entry-level borrowing capacity.

How much did home lending fall after interest rates rose?

The RBA raised the cash rate 13 times between May 2022 and November 2023, from 0.10% to 4.35%. Total new lending fell from $349 billion in 2021 to $279 billion in 2023. First home buyers were hit hardest, with their share of total new lending falling from 26% in 2020 to around 18% by 2025 as borrowing capacity declined.

In 2025, there were 556,092 new loan commitments for owner-occupier and investor dwellings combined, excluding refinancing. Of these, 119,464 were first-home buyer loans. By value, total commitments reached $385 billion. The December 2025 quarter alone recorded 149,434 commitments worth $108.3 billion, a quarterly record.

In 2025, 119,464 first-home buyers took out a new loan, excluding refinancing, borrowing a combined $67.9 billion. The pandemic year of 2021 was the modern peak, when 162,808 first-home buyers borrowed $73.3 billion. First-home buyers made up 26% of total new lending in 2020, but their share has since settled at around 18%.

Section 04Interest rates

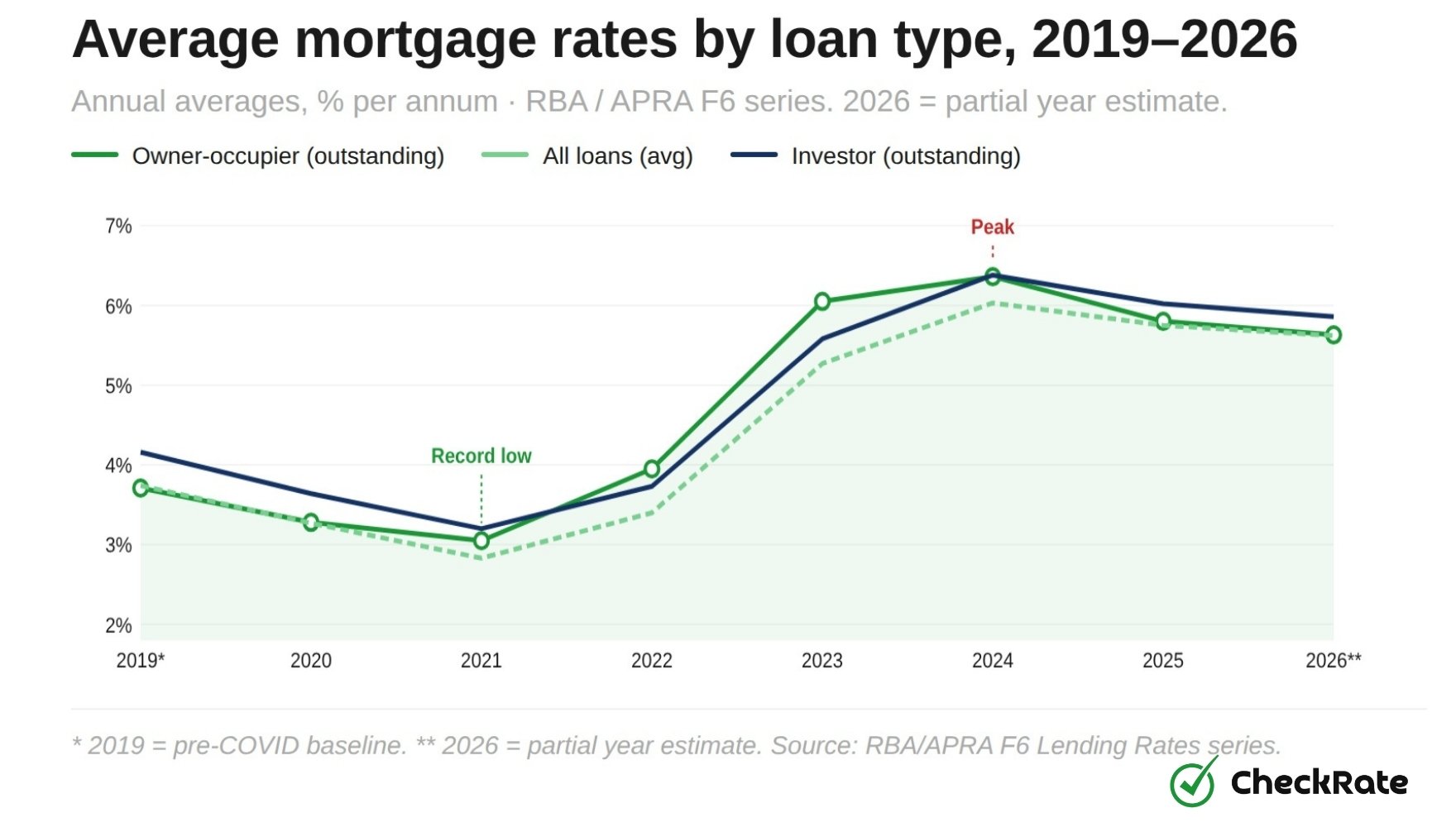

Mortgage interest rates from 2019 to 2026

The average rate on outstanding owner-occupier loans fell to around 2.63% by mid-2021, before the RBA’s tightening cycle pushed it above 6% by mid-2024. By February 2026, that rate had eased to 5.62% after RBA cash rate cuts in 2025 and early 2026. Rates on newly written loans moved closely with outstanding rates, reaching 5.61% in the same month.

Investor loans have consistently attracted rates around 0.20 to 0.30 percentage points higher than comparable owner-occupier loans throughout the cycle. That gap reflects lender risk weighting and APRA capital requirements, and it has remained in place even as rates have fallen from their peak.

Average mortgage interest rates, Australia

Annual averages, % per annum · RBA / APRA F6 series, 2019–2026

OO variable rate

OO all loans

Investor all loans

2019 covers July–December only. 2026 covers January–February only. Rates are weighted averages of APRA-reporting institutions covering more than 95% of housing credit.

Source: APRA / RBA Housing Lending Rates (F6), publication date 9 April 2026.

Did you know

The outstanding mortgage rate is the average across existing loans, including older fixed-rate loans from 2020–21. The new loan rate reflects what borrowers are being offered now. In 2022–23, new loan rates rose faster because many existing borrowers were still on fixed terms. Now that most of those fixed periods have ended, the two rates sit much closer together.

As of February 2026, the average rate on outstanding owner-occupier mortgages was 5.62% per annum, down from a peak of around 6.11% in mid-2024. The average rate on new loans was 5.61%. Variable-rate loans averaged 5.63%, while outstanding investor loans averaged 5.86%.

The average rate on outstanding owner-occupier mortgages rose from a low of around 2.63% in mid-2021 to around 6.11% by mid-2024, an increase of 3.48 percentage points. On a $600,000 loan over 30 years, that rate increase would add roughly $1,300 per month in repayments. For the average new loan of $736,000, the increase would be closer to $1,500 per month.

Section 05Costs by state

Which states have the highest mortgage costs?

Mortgage costs vary widely across Australia, both in dollar terms and as a share of household income. NSW mortgage holders had the highest average weekly housing costs at $574 per week, equal to 17% of gross household income. The ACT and NT followed at $546 and $534 per week. Tasmania recorded the lowest average at $346 per week, less than two-thirds of the NSW figure.

In Australia, mortgage stress is commonly measured as spending 30% or more of gross household income on housing costs. No state average exceeded that level in the 2019–20 data, but averages can hide large differences within each state.

Mortgage burden by state and territory

ABS Housing Occupancy and Costs, 2019–20

NSW

$574/wk

ACT

$546/wk

NT

$534/wk

VIC

$501/wk

QLD

$447/wk

WA

$443/wk

SA

$390/wk

TAS

$346/wk

Figures cover owner households with a mortgage at time of survey. Weekly housing costs include mortgage repayments, council and water rates, and body corporate fees.

Source: ABS Housing Occupancy and Costs, 2019–20.

Data note: mortgage costs reflect 2019–20 rates

The 2019–20 survey data above reflects a low-rate period, when the average outstanding mortgage rate was around 3.3%. By 2024, rates had peaked above 6%, increasing weekly repayments and the share of income going to housing costs. Updated state-level cost data is not yet available because the ABS 2023–24 Survey of Income and Housing results were not released due to data quality concerns. The next results are expected from mid-2027.

NSW had the highest average weekly housing cost in 2019–20 at $574 per week, as well as the highest income share at 17%. The ACT had the highest median outstanding mortgage debt at $347,000, while the NT had the highest share of households with a mortgage at 43%. Tasmania was lowest on all three measures.

The widely used mortgage stress benchmark is 30% of gross household income spent on housing costs. In the 2019–20 data, state averages for mortgaged households ranged from 14% in SA and WA to 17% in NSW, all below the 30% threshold.

Section 06Affordability

How long does it take to save a deposit?

In 2017, a single income earner saving 4.7% of their income needed around 25 years to save a 20% deposit on the national median dwelling. By 2025, with the median dwelling price at $825,000 and a saving rate of 6.9%, that figure was roughly 21 years.

Changes in the saving rate can make a large difference to deposit timelines. When household savings spiked to 13.9% during COVID restrictions in 2020, the deposit timeline fell to around 8.3 years nationally. That was not because housing became more affordable: household spending was lower during lockdowns. Once saving dropped back toward 3–4% in 2022–23, the years-to-save figure rose to its highest level on record before settling again as saving rates normalised.

$825k

What is the median dwelling price in Australia?

In 2025, the national median dwelling price was $825,000, up from $465,000 in 2015. Sydney was much higher at $1.515 million, Brisbane had passed $1.1 million, and Perth reached $951,000. Only Darwin and regional NT remained below $750,000 among capital and near-capital markets.

Deposit savings reality, 2025

21yrs

Years to save a 20% deposit nationally on a single income (2025)

8.3yrs

Best recent year was 2020, a pandemic saving spike, not an affordability gain

39yrs

Years to save a 20% deposit in Sydney on a single income (2025)

18×

Sydney median multiple (house price to income ratio)

Single average income ($111,815) at 6.9% saving ratio. 20% deposit on median dwelling price.

How these figures are calculated

Years to save = 20% of median dwelling price divided by annual saving capacity. Annual saving capacity is the 2025 average annual income ($111,815 nationally) multiplied by the 2025 household saving ratio (6.9%). These figures are illustrative. Actual timelines vary by income, household size, location and whether government schemes such as the First Home Super Saver Scheme or the First Home Guarantee are used.

Using the 2025 national saving ratio of 6.9% and average income, saving a 20% deposit on a median-priced dwelling takes about 21 years nationally. That rises to 39 years in Sydney and falls to 19 years in Darwin. Government schemes such as the First Home Guarantee, which allows a 5% deposit, and the First Home Super Saver Scheme can reduce the timeline for eligible buyers.

Yes. The estimated time needed to save a 20% deposit rose from around 6 years nationally in 2000 to roughly 21 years by 2025. Much of the recent increase occurred between 2020 and 2023, when dwelling prices rose and saving rates fell from their pandemic highs.